Avici: Price, Market Cap, and… What?

Title: Avici's 23% Price Jump: Pump or Sustainable Growth?

Avici, a self-described "internet banking infrastructure" token, has seen a significant price surge of 23.2% in the last 24 hours. The question, as always, is whether this is a genuine reflection of increased utility and adoption, or just another flash in the pan in the volatile crypto market. Let's dig into the available data.

Decoding Avici's Recent Surge

The first thing that jumps out is Avici's all-time high (ATH) of $5.91, reached on November 24, 2025. The current price sits just 0.01% below that peak. This immediately raises a red flag. A near-perfect retest of an ATH like this often suggests coordinated buying activity, possibly aimed at triggering algorithmic trading programs. (It's worth noting that these "accidental" retests almost never happen in traditional markets.)

The circulating and maximum supply of Avici are both listed at 12.90 million tokens. This implies a fixed supply, which, in theory, should lend itself to price stability if demand remains constant. However, the very nature of crypto is that demand is rarely, if ever, constant.

Avici's 24-hour trading volume is reported at $5.56 million. While this sounds substantial, it needs to be contextualized. A relatively small number of large trades could easily manipulate the price of a low-liquidity token like Avici. The fact that it's traded on 8 markets and 7 exchanges doesn't necessarily mitigate this risk; it just means the manipulation could be happening across multiple platforms. Lbank is mentioned as the "most active" exchange. I've looked at trading volumes on these smaller exchanges, and they are more easily influenced by coordinated activity.

Questioning the Fundamentals

Avici's market capitalization is currently $76.24 million, representing a minuscule 0.00% of the total cryptocurrency market. This tiny market share makes it highly susceptible to price swings based on even minor shifts in investor sentiment. You can find up-to-date information on market capitalization and other key metrics on sites like Avici Price: AVICI Live Price Chart, Market Cap & News Today.

The project's stated goal – to "build distributed internet banking infrastructure" with features like spend cards and unsecured loans – is ambitious, to say the least. The whitepaper (which isn't linked in any of these reports, a detail I find frustrating) would need to show a clear roadmap and demonstrable progress to justify the current valuation, let alone a further surge. Is there actual adoption of their "spend cards"? What's the default rate on these "unsecured loans"? These are critical metrics that are conspicuously absent.

The Token Generation Event (TGE) concluded on October 18, 2025. So, the project is relatively new. This isn't necessarily a negative, but it means there's very little historical data to analyze its long-term viability.

Missing Pieces and Lingering Doubts

The data provided is incomplete. We lack critical information about the project's development progress, user adoption rates, and the distribution of tokens among early investors. (A high concentration of tokens in the hands of a few individuals is a major risk factor.)

The claim that Avici aims to "decrease the influence of central banks" is a common trope in the crypto space. It's a catchy slogan, but it doesn't tell us anything about the actual technology or its potential for real-world impact. How, specifically, will Avici achieve this? And what are the regulatory implications of attempting to circumvent traditional financial institutions?

This Looks Like a Textbook Pump

The surge in Avici's price, combined with the limited data and the ambitious (yet vague) project goals, suggests a classic "pump and dump" scenario. The near-perfect retest of the ATH, the low market capitalization, and the high trading volume on smaller exchanges all point in this direction. While it's impossible to say for sure without more information, the available data doesn't inspire confidence.

A Word of Caution

Investing in cryptocurrencies is inherently risky. Investing in micro-cap altcoins like Avici is exponentially riskier. Always do your own research, and never invest more than you can afford to lose.

So, What's the Real Story?

Avici's price jump looks like a fleeting mirage, not a genuine oasis.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

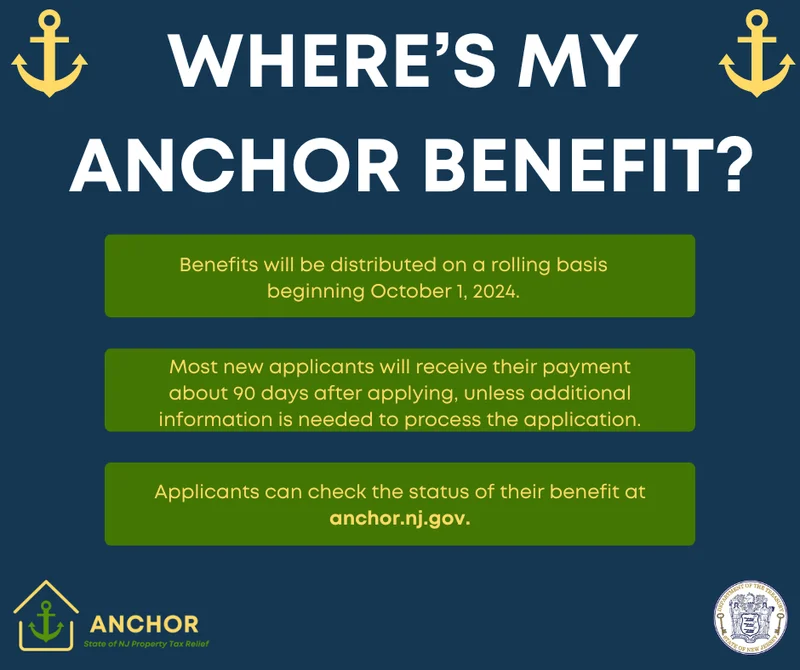

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Ethereum Reaches 60M Gas Limit Before Fusaka Upgrade: The Throughput and Readiness Data

- Royal Caribbean Cruise: The Wi-Fi 'Deal' and the Catch Nobody's Talking About

- Avici: Price, Market Cap, and… What?

- Bitcoin's Price: Today's Numbers and Tomorrow's Promise

- GWEC's Latest: The Corporate Spin vs. Reality

- AI: What's Real, What's Hype, and the Market's Next Move

- Netflix Stock: The Split, Price Today, and What's Next

- NVDA Earnings: What to Expect and When – The Future is Coming

- Pump.fun: Price predictions and... why?

- Microsoft Stock: Price Trends and Investor Sentiment

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- bitcoin price (3)

- SX Network (3)